[ad_1]

Thomas Coesfeld is the Chief Monetary Officer of BMG. Right here, in an unique MBW op/ed, Coesfeld argues that the right response to booming international music business revenues ought to be improved service to artists and songwriters – somewhat than a money-no-object pursuit of market share…

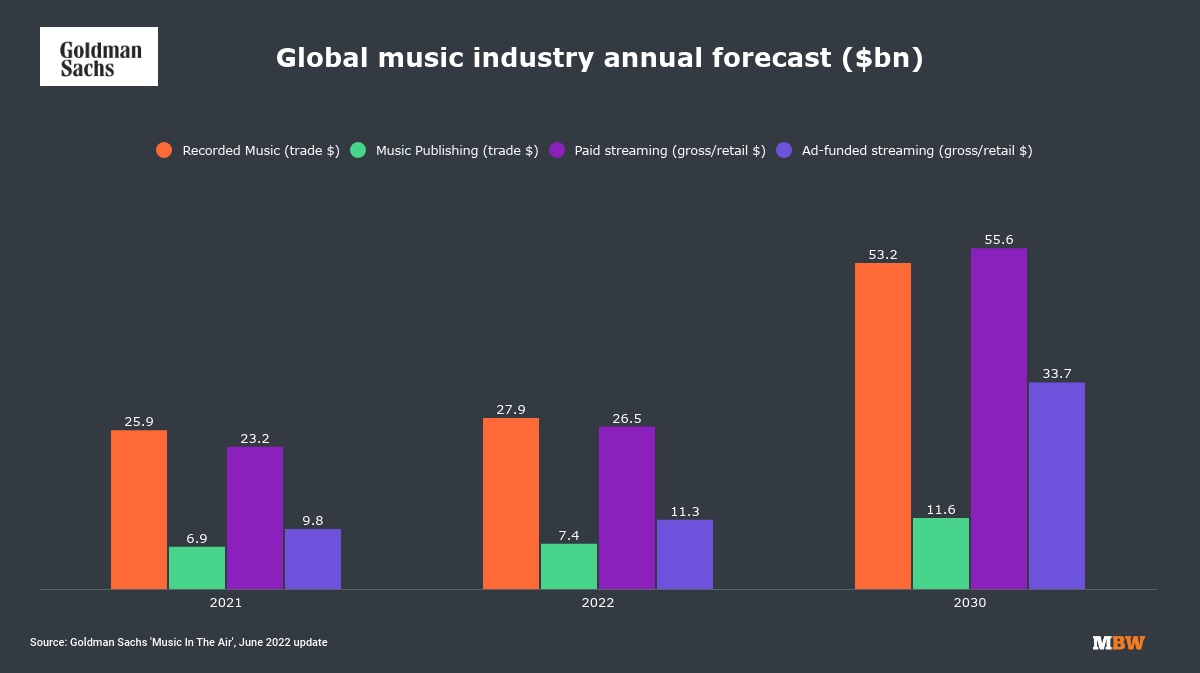

June 13, 2022 was a giant day for finance groups throughout the music business. It was the day Goldman Sachs released its revised forecasts for the music business with new numbers suggesting the recorded music market will double by the tip of the last decade.

At BMG, as little question elsewhere, inner forecasts had been quickly being upgraded. These with lengthy recollections who noticed the vinyl LP eclipsed by compact discs promoting for twice the worth could possibly be forgiven for pondering historical past was repeating itself. Completely satisfied days!

Nonetheless, regardless of the rosy image painted by Goldman’s forecasts, there are grounds for just a little humility. Nothing in these forecasts suggests the expected development can be in any sense because of the collective efforts of music corporations themselves.

They aren’t based mostly on document corporations out of the blue getting higher at their jobs and signing extra or greater hits; they’re a by-product of a elementary shift in the way in which customers select to devour music, pushed by the funding and innovation of DSPs.

It’s cheap due to this fact to debate what the right response is to this stroke of excellent fortune.

If the previous is any information, the default response can be to do extra of the identical – solely extra expensively – within the pursuit of market share. It’s laborious to argue {that a} battle for market share advantages both artists or songwriters. Historical past suggests it doesn’t do a lot for shareholders both.

On the idea of the outdated truism that one of the best time to repair the roof is whereas the solar is shining, I’d argue that the actual battleground shouldn’t be on marketshare, however on service and value-add to musicians and rightsowners.

“Higher aligning the pursuits of music corporations with the artists and songwriters they serve is, I consider, the only most essential transformational alternative provided by streaming.”

Enhancing service ranges, higher aligning the pursuits of music corporations with the artists and songwriters they serve is, I consider, the only most essential transformational alternative provided by streaming.

The primary part of that transformation centered on equity and transparency, a recognition that the historic relationship of music corporations to musicians was unbalanced and sometimes unfair and that merely translating the contractual phrases of the analogue period to streaming was inappropriate and unsustainable.

A lot of the business has now accepted in phrase if not all the time in deed that equity and transparency are non-negotiable within the streaming age.

The second part, which we’re presently in the course of, is the rising understanding that music corporations are actually basically service companies to musicians. They’re now not the principals available in the market. They work for the artists and songwriters who truly make the music.

Progress right here is slower. Understandably the bigger the corporate, the much less eager they’re to simply accept that their historic position because the drivers of the enterprise is over. However that’s the unavoidable logic of the know-how.

The third transformation arising out of the earlier two, we consider, can be a deal with the lively income administration of recorded and publishing rights, minimising inefficiencies within the income chain and maximising earnings to rights homeowners.

The important thing driver for this would be the growing variety of high-value catalogues held exterior the normal music corporations – both owned by artists themselves or, more and more, by buyers.

“Traders who’ve dedicated actually billions of {dollars} to buying music IP won’t tolerate the diploma of income leakage, the a number of commissions, admin charges and grindingly gradual processes nonetheless frequent on this enterprise.”

Definitely buyers who’ve dedicated actually billions of {dollars} to buying music IP won’t tolerate the diploma of income leakage, the a number of commissions, admin charges and grindingly gradual processes nonetheless frequent in a enterprise which has nonetheless but to made the leap from an analogue to a digital mindset.

It calls for a deal with music business buildings and overhead on the one hand and processes on the opposite. It’s going to put an growing premium on probably the most under-appreciated providers of the music business – copyright, royalties, earnings monitoring. They could not have the glamour of A&R, advertising and marketing or synch, however they are going to be core differentiators within the years forward.

We’d somewhat pin our hopes on differentiation and a transparent technique somewhat than merely hoping we will coast our technique to elevated revenues on the again of market development. There may be a lot work nonetheless to be completed.

In a current pitch to a songwriter we reviewed a possible shopper’s Prime 30 tracks on YouTube – solely three of them had been appropriately registered and claimed by their present music writer.

This isn’t an remoted case. Putting offers with digital platforms is one factor; figuring out how then to work with them efficiently is one thing else completely. It’s these areas of income optimisation and earnings monitoring assurance the place we consider the best alternative lies.

We should make sure that as a lot as potential of the top-line development forecast by Goldman Sachs is captured and handed on somewhat than squandered on goals akin to market share which imply nothing to the musicians who in the end pay the payments.

That’s one of the best ways for us to repay the religion of the artists, songwriters and naturally shareholders who in the end make the work all of us do potential.

To place it one other manner, if that isn’t our precedence, artists and songwriters and rightsowners could possibly be forgiven for asking what’s the level of music corporations in any respect?Music Enterprise Worldwide

Source link